On Decentralized Network Equity (Part I)

Thoughts on structuring decentralized revenue-sharing rights, yield-bearing tokens, and other forms of network equity under Senate and House versions of market structure legislation

While market structure legislative attempts have become mired in debates over stablecoin yield distribution, tokenized securities, developer protections and conflicts of interest, one topic of legislation that has received significantly less fanfare has the potential to fundamentally alter the way defi projects think about economic flows, and the way users engage with networks: namely, the implementation of decentralization as a limitation on the application of the US securities regime.

Both the House-passed CLARITY Act and the January 2026 Senate Banking Committee substitute create pathways for tokens with genuine economic rights, what I refer to as “network equity,” to be issued and traded without securities registration. This article seeks to provide practical guidance on how to structure token economics and initial issuance to take advantage of these frameworks and to position clients accordingly if/when market structure legislation is enacted.

The core insight practitioners should internalize: both bills permit tokens to have substantial economic rights derived from network operations without becoming securities. The key determinant is the locus from which those economic rights issue- the decentralized system itself, not promises from a centralized team.

This Part I will discuss the definitional framework (along with a critical ambiguity) enabling network equity. Part II will review potential pathways to issuance of network equity tokens.

The Decentralized Network Equity Token Definitional Framework (Senate)

The current Senate draft uses the “network token” / “ancillary asset” framework. Understanding how a decentralized network equity token escapes securities law requires following the statutory logic step-by-step.

Step 1: Digital Commodities Are Not Securities

The foundation is straightforward: the bill amends the definition of “security” across federal securities statutes to exclude digital commodities, including Section 109 which amends the Securities Investor Protection Act of 1970 to add: “[t]he term ‘security’ does not include a digital commodity.”

This is the exit ramp. If an asset qualifies as a “digital commodity,” it is categorically excluded from the securities laws.

Step 2: Network Tokens Are Digital Commodities

Section 4B(a)(6)(A) defines a “network token” as:

“[A] digital commodity that is intrinsically linked to a distributed ledger system and that derives, or is reasonably expected to derive, its value from the use of such distributed ledger system, and, pursuant to the Digital Asset Market Clarity Act and the amendments made by the Digital Asset Market Clarity Act, is treated as a non-security solely for purposes of the Federal securities laws.”

Section 4B(b)(1) operationalizes the above, providing that “a network token shall be treated as a non-security” for purposes of the Securities Act, Exchange Act, Investment Company Act, Investment Advisers Act, SIPA, and preempts inconsistent state law.

The pathway: Network Token → Digital Commodity → Not a Security.

Step 3: Disqualifying Financial Rights — What Kicks You Out of “Network Token” Status

Section 4B(a)(6)(B) provides that the term “network token” does not include certain assets. A token is disqualified if it “represents, gives the holder, or is substantially economically or functionally equivalent to”:

(I) “A debt or equity interest, or an option on a debt or equity interest, in a person.”

(II) “Liquidation rights with respect to a person.”

(III) “An entitlement to, or a reasonable expectation of, an interest, dividend, or other payment, or direct or indirect transfer of value, from a person (other than a decentralized governance system).”

(IV) “An express or implied financial interest in (including a limited partnership interest or interest in intellectual property of), or provided by, a person (other than a decentralized governance system).”

The Pattern: Every disqualifying right requires a relationship to a person. The statute distinguishes between rights tied to legal persons (corporations, foundations, individuals) and rights tied to decentralized governance systems.

Step 4: The Decentralized Governance System Carveout

The parenthetical in (III) and (IV) “(other than a decentralized governance system)” represent the critical carveouts.

Payments or financial interests flowing from a decentralized governance system do not constitute disqualifying financial rights. A “decentralized governance system” is defined in Section 2(5)(A) as “any transparent, rules-based system permitting persons to form consensus or reach agreement in the development, provision, publication, maintenance, or administration of such distributed ledger system, in which participation is not limited to, or under the effective control of, any person or group of persons under common control.”

Defining “Common Control” in the Senate Framework

The DGS definition requires that participation not be “under the effective control of, any person or group of persons under common control.” Unlike the House bill, the Senate explicitly addresses how “common control” will be defined.

Section 2(4): The definitions section provides that “the term ‘common control’ has the meaning given the term by the Commission pursuant to rules promulgated under section 104(b).”

Section 104(b) Rulemaking: The SEC is directed to promulgate rules defining when a distributed ledger system is “under common control by related persons,” based on specific statutory criteria:

(A) Open Digital System: Whether the protocol is freely and publicly available via open-source code

(B) Permissionless and Credibly Neutral: Whether any person or group has unilateral authority to restrict, censor, or prohibit use, or has private permissions/hard-coded privileges providing preferential treatment

(C) Distributed Digital Network: The extent to which a person or group has beneficial ownership of 49% or more of outstanding units

(D) Autonomous System: Whether the system has reached an autonomous state and whether any person has unilateral authority to alter functionality

(E) Economic Independence: Whether primary programmatic mechanisms for value accrual are functional

Key Difference from House: The Senate explicitly delegates “common control” definition to SEC rulemaking rather than providing a statutory bright-line threshold. The 49% ownership figure in criterion (C) is one factor for the SEC to consider, not a definitive threshold. Section 104(b)(3) further directs the SEC to establish safe harbors for when a system is not under common control.

Practitioner Implications:

• The Senate framework contemplates that “common control” will be a multi-factor analysis rather than a single ownership threshold

• The 49% ownership criterion is considerably higher than the House’s 20% threshold (for “mature” chains, but not necessarily DGS, as further discussed below), suggesting the Senate may tolerate more concentrated ownership if other factors (open source, permissionless, no unilateral control) are satisfied

• Until SEC rulemaking is complete, practitioners face uncertainty about what level of coordination or ownership concentration defeats DGS status

• Conservative advice: structure to satisfy all enumerated criteria-open source, no unilateral control, distributed ownership, functional value mechanisms

Step 5: The Rule of Construction

Section 4B(a)(6)(C) provides an additional safeguard:

A digital commodity ... shall not be disqualified from being deemed a network token due to the granting of economic interests or voting capabilities with respect to a distributed ledger system or its decentralized governance system, as further clarified by the Commission through the final rule adopted under section 105.

This is explicit statutory text: even if a token grants “economic interests” in the protocol or governance system, that does not disqualify it from being a network token.

Step 6: Section 105 - The Mandatory Savings Clause

Section 105 is the capstone. It mandates the SEC to adopt regulations confirming that a network token “shall not be considered as providing a disqualifying financial interest” if its value is primarily derived from the distributed ledger system, including where:

(A) “The mechanisms of the distributed ledger system collect, receive, accrue, or distribute consideration from the functioning of the distributed ledger system.”

(B) “The network token provides governance capabilities with respect to a distributed ledger system or a decentralized governance system.”

(C) “The value of the network token appreciates or depreciates due to the use of, or in response to the efforts, operations, or financial performance of, the distributed ledger system ... or its decentralized governance system.”

(D) “For a network token that meets the definition of an ancillary asset, the value of the network token appreciates or depreciates due to the efforts of the ancillary asset originator or related person.”

Senate Logic Chain Summary:

Token intrinsically linked to DLS + value from system use → Network Token → No disqualifying financial rights (payments/interests from DGS are carved out) → Digital Commodity → Not a Security

The House Framework

The House CLARITY Act uses a different architecture centered on “digital commodities,” “investment contract assets,” and “mature blockchain systems.” The logic chain reaches the same destination through different steps.

Step 1: Digital Commodities Are Not Securities

Section 301 amends the definition of “security” across federal securities statutes. The Securities Act and Exchange Act are amended to provide: “The term [security] does not include a digital commodity.”

This is the same exit ramp as the Senate: if an asset is a “digital commodity,” it’s categorically excluded from securities law.

Step 2: What Is a Digital Commodity?

Section 103 amends the Commodity Exchange Act to define “digital commodity” at new Section 1a(16)(F):

[A] digital asset that is intrinsically linked to a blockchain system, and the value of which is derived from or is reasonably expected to be derived from the use of the blockchain system.

A digital asset is “intrinsically linked” if it is “directly related to the functionality or operation of the blockchain system or to the activities or services for which the blockchain system is created or utilized.” The statute provides an illustrative list including: issued by the system’s programmatic functioning; used to transfer value; used to access services; used for governance; used to pay fees or validate transactions; used as payment or incentive to participants.

Step 3: Exclusions from Digital Commodity -The Disqualifying Rights

Section 1a(16)(F)(iii) provides that “digital commodity” does not include certain assets. The critical exclusion is at (I), covering securities:

A note, an investment contract, or a certificate of interest or participation in any profit-sharing agreement that:

(AA) represents or gives the holder an ownership interest or other interest in the revenues, profits, obligations, debts, assets, or assets or debts to be acquired of the issuer of the digital asset or another person (other than a decentralized governance system);

(BB) makes the holder a creditor of the issuer of the digital asset or another person; or

(CC) represents or gives the holder the right to receive interest or the return of principal from the issuer of the digital asset or another person.

The Pattern: Like the Senate bill, the House exclusions focus on interests in or payments from a person. And critically, (AA) contains the same carveout: “(other than a decentralized governance system).”

Step 4: The Decentralized Governance System Carveout

The House bill defines “decentralized governance system” in Section 2(a)(24) of the Securities Act (as amended) identically to the Senate:

Any transparent, rules-based system permitting persons to form consensus or reach agreement in the development, provision, publication, maintenance, or administration of such blockchain system, where participation is not limited to, or under the effective control of, any person or group of persons under common control.

Step 5: Investment Contract Assets

Section 201 introduces a separate concept: the “investment contract asset.” This is defined as a digital commodity that “can be exclusively possessed and transferred, person to person, without necessary reliance on an intermediary, and is recorded on a blockchain” and is “sold or otherwise transferred ... pursuant to an investment contract.”

The statute then amends the definition of “investment contract” across all securities statutes to add: “The term ‘investment contract’ does not include an investment contract asset.”

What This Means: Even if a token was originally sold as part of an investment contract (the Howey concern), the token itself is not the investment contract. The token is an “investment contract asset” - excluded from the investment contract definition, making it a digital commodity, thus a non-security.

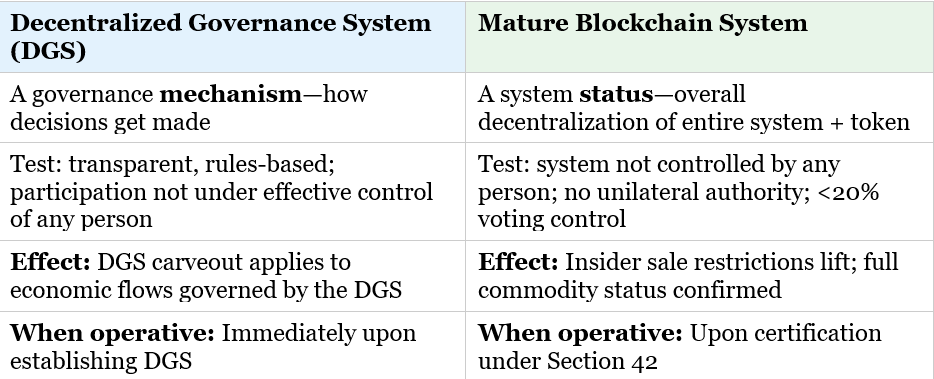

Step 6: Mature Blockchain Systems—Distinct from DGS

Section 2(a)(31) defines a “mature blockchain system” as “a blockchain system, together with its related digital commodity, that is not controlled by any person or group of persons under common control.”

This is conceptually distinct from a decentralized governance system, and practitioners should understand the difference:

Consequences of Failing to Achieve Maturity: Section 4B(e) imposes serious consequences if the blockchain system does not become mature within the 4-year window (subject to SEC extensions):

1. Primary Issuance Shuts Down: The SEC “may not permit any additional reliance on an exempt offering” unless the Commission has qualified the offering statement, essentially requiring a Reg A+ style review process for any future issuance.

2. Enhanced Disclosure Obligations: Issuers must provide detailed explanations of why maturity wasn’t achieved, future development plans, and material risk factor disclosures. Transaction reporting and beneficial ownership disclosure obligations apply to related/affiliated persons.

3. Insider Restrictions Continue: The sale restrictions applicable to digital commodity affiliated persons and related persons remain in effect indefinitely.

Important Distinction: Failure to achieve maturity does not appear to cause the token to lose digital commodity status or become a security. The “investment contract asset” exclusion remains operative, and Section 203’s protection for secondary market transactions by non-issuers should still apply. The consequences fall primarily on the issuer and insiders, not on the token’s classification or secondary market trading by ordinary holders.

Key Question: Can a protocol have a DGS without being “mature?”

Answer: Yes, but with an important caveat

Example: A protocol launches with genuine DAO governance-transparent rules, open participation, no single party controls the voting process. That’s a DGS, definitionally. But founders still hold 25% of tokens, the development company holds admin keys for emergency upgrades, and the core team can effectively coordinate 30% of validator power. The governance mechanism is decentralized (DGS exists), but the overall system isn’t mature because persons still have control over aspects of the system.

Critical Drafting Ambiguity: Does the 20% Threshold for Mature Blockchains Apply to DGS?

Practitioners should be aware of a potentially significant drafting ambiguity regarding the relationship between the mature blockchain criteria and the DGS definition.

The Textual Issue: Both definitions use the phrase “persons under common control,” but only Section 42(c)(2)(E) (setting forth the requirements necessary for a blockchain to be deemed “mature”) provides a concrete threshold-the 20% voting power limit. The DGS definition in Section 2(a)(24) uses the phrase “effective control” and “common control” without defining either term or cross-referencing Section 42.

DGS Definition (Section 2(a)(24)):

participation is not limited to, or under the effective control of, any person or group of persons under common control

Mature Blockchain Criteria (Section 42(c)(2)(E)):

No person or group of persons under common control (i) has the unilateral authority... to control or materially alter the functionality... or (ii) has the unilateral authority to direct the voting, in the aggregate, of 20 percent or more of the outstanding voting power...

Arguments that 20% is limited to maturity certification:

• Textual placement: the threshold appears only in Section 42, which governs mature blockchain determinations

• Different operative terms: DGS uses “effective control”; Section 42(c)(2)(E) uses “unilateral authority”

• Different functions: DGS carveout protects specific economic flows; maturity unlocks insider sales-different purposes potentially warrant distinct thresholds

• If drafters intended 20% to define “common control” globally, they could have placed it in Section 2’s definitions

Arguments that 20% might inform DGS analysis:

• Statutory interpretation canon: same terms in the same statute generally carry the same meaning

• The 20% provides the only concrete, administrable threshold for “common control” anywhere in the bill

• Without it, “effective control” and “common control” in the DGS definition are undefined and potentially unworkable

• Courts might look to Section 42 as evidence of congressional intent about what level of control is disqualifying

Practical Example: A DAO has transparent, rules-based governance with open participation. But three affiliated VCs collectively hold 25% of governance tokens and typically vote together.

Under narrow reading (20% only for maturity): The DGS inquiry is whether participation is under “effective control”- a facts-and-circumstances test. 25% coordinated voting might still allow DGS status if other participants can meaningfully participate and outcomes aren’t predetermined.

Under broad reading (20% informs DGS): If the 20% threshold applies to DGS, then >20% coordinated control means no DGS, thus no carveout, resulting in protocol fee distributions being deemed disqualifying financial rights.

The Stakes: If the DGS carveout doesn’t apply, protocol fee distributions could constitute “payments from a person” and disqualify the token from digital commodity status entirely.

Practitioner Guidance on the Ambiguity:

1. Flag the ambiguity in client advice. This is an open question that SEC/CFTC rulemaking or litigation may eventually resolve

2. Conservative approach: Structure to satisfy both readings. Aim for <20% coordinated control to ensure DGS status under either interpretation

3. Document the analysis: If relying on the narrow reading (>20% coordinated but still claiming DGS), document why “effective control” is not present despite concentrated holdings (e.g., active participation by other holders, unpredictable voting outcomes, no formal coordination agreements)

4. Watch for rulemaking: Both bills direct agency rulemaking that may clarify these thresholds

House Logic Chain Summary:

Token intrinsically linked to blockchain + value from system use → No exclusions (interests in/from DGS carved out- operative immediately) → Digital Commodity → Not a Security. Maturity certification unlocks insider liquidity, permits continued exempt offerings, and reduces disclosure burden- but failure to achieve maturity does not appear to change the token’s digital commodity status.

Key Insight: Both bills draw the same fundamental line. Economic rights flowing from a protocol or decentralized governance system do not disqualify a token, and this protection is immediate upon establishing a qualifying DGS. Economic rights flowing from a legal person (corporation, foundation, individual) may disqualify. Under the House bill, maturity/certification determines (1) whether insiders can sell freely, (2) whether the issuer can continue exempt primary offerings, and (3) the level of ongoing disclosure burden, but failure to achieve maturity does not appear to change the token’s underlying commodity status.

Economic Features That Pass / Fail Both Frameworks

1. Protocol Fee Distribution

Structure: Smart contract collects fees from protocol usage and distributes to token holders/stakers.

Senate Analysis: Section 105(a)(1)(A) confirms “mechanisms of the distributed ledger system collect, receive, accrue, or distribute consideration.” Distribution from DGS is carved out of disqualifying rights.

House Analysis: Value “derived from the use of the blockchain system.” Ownership interest in revenues of a DGS is carved out at (AA). Programmatic distribution from protocol code qualifies.

Practitioner Implications: Fee switches may be permissible under both frameworks from day one if governed by a DGS. Ensure distribution mechanism is encoded in protocol or controlled by DAO or decentralized governance -not discretionary decisions of a foundation.

2. Governance Voting Rights

Structure: Token grants voting rights over protocol parameters, treasury, upgrades.

Senate Analysis: Section 105(a)(1)(B) confirms “governance capabilities with respect to a distributed ledger system or a decentralized governance system.” Rule of Construction protects “voting capabilities.”

House Analysis: CEA definition includes tokens “used to participate in the decentralized governance system of the blockchain system.” Governance is an enumerated qualifying use.

Practitioner Implications: Governance tokens are protected under both frameworks. Distinguish governance over the protocol (permitted) from governance over a corporate entity (potentially disqualifying).

3. Value Appreciation from Network Growth

Structure: Token value correlates with network metrics, e.g. TVL, transaction volume, user adoption.

Senate Analysis: Section 105(a)(1)(C) confirms value appreciation “due to the use of, or in response to the efforts, operations, or financial performance of, the distributed ledger system.”

House Analysis: Digital commodity definition requires value “derived from or is reasonably expected to be derived from the use of the blockchain system.” Value from system performance is the definition itself.

Practitioner Implications: Tokenomic design advice should emphasize value accrual tied to onchain metrics. Avoid marketing emphasizing team efforts as the source of value.

4. DAO Treasury Distributions

Structure: DAO accumulates treasury from protocol revenue; governance votes determine distributions.

Both Frameworks: Distributions from a “decentralized governance system” are explicitly carved out of disqualifying rights in both bills. Both define DGS identically: transparent, rules-based, not under effective control of any person.

Practitioner Implications: Ensure the DAO (or other dispersed governance) actually qualifies as a DGS. Document decentralization: voting power distribution, open participation, no effective control by founders or affiliated groups. This protection will be available immediately (if language left unchanged) - no need to wait for system-wide maturity.

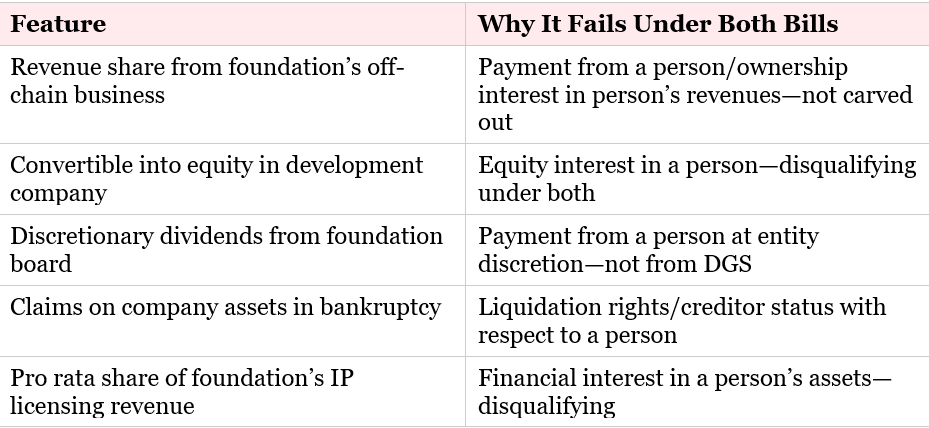

5. Features That Fail Both Frameworks

Conclusion: The Definitional Framework for Network Equity

Both the Senate and House frameworks establish a coherent (and nearly identical) pathway for tokens with genuine economic rights to exist outside the securities laws. The core logic is consistent across both bills:

- Digital commodities are categorically excluded from the definition of “security.”

- Tokens intrinsically linked to a blockchain/distributed ledger system, deriving value from its use, qualify as digital commodities, provided they do not carry disqualifying financial rights.

- Disqualifying rights are defined by reference to legal persons. Debt or equity interests in a person, liquidation rights with respect to a person, payments from a person- all disqualify. The consistent textual pattern draws a bright line between entity-level economics and protocol-level economics.

- The DGS carveout as the linchpin. Both bills explicitly provide that economic interests flowing from a “decentralized governance system” do not constitute disqualifying financial rights. This is what enables network equity-protocol fee distributions, DAO treasury allocations, governance-controlled buybacks-to coexist with non-security status.

- The DGS carveout is operative immediately. Unlike maturity certification (House) which affects issuer conduct and insider liquidity, the DGS carveout goes to the token’s fundamental classification.

The critical ambiguity practitioners should flag: what level of coordinated ownership or control defeats DGS status? The Senate delegates this to SEC rulemaking with a multi-factor framework. The House provides a 20% voting threshold for maturity certification, but whether that threshold informs the DGS analysis is textually unclear. Conservative advice is to structure for both readings: aim for sub-20% coordinated control, open-source code, no unilateral authority, and functional programmatic mechanisms.

With this definitional framework established, Part II will turn to the practical question: how do decentralized network equity tokens actually get into the hands of users? We will examine the issuance pathways available under both bills: gratuitous distributions, the House Section 4(a)(8) retail exemption, private placement with secondary market treatment, the Senate’s Regulation Crypto framework, and the “fee-switch” for protocols with tokens already “in the wild”: as well as the insider sale restrictions that apply during the path to decentralization.

The legislation is not yet law, and significant rulemaking will be required to fill gaps. But the potential structural framework is clear: tokens can have real economic value, trade freely to retail, and function as “network equity” - if designed and issued appropriately.