How to Launch (or Activate) a Decentralized Network Equity Token Under Pending Crypto Legislation

Part II: Issuance Pathways Under the CLARITY Act and Senate Market Structure Bills

Part I of this three-part series addressed the definitional framework; this Part discusses issuance pathways, certification processes, and post-TGE activation of economic rights. Part III will set forth a decision framework, a DGS checklist and five model approaches to token issuance and will be available under a soon-to-be-announced paid sub tier intended for professional advisors (note: 100% of sub revenue will be donated to crypto advocacy groups).

First off: Why Analyze Launch Pathways Under a Law That Doesn’t Yet Exist?

A reasonable question: why devote practitioner attention to the mechanics of launching tokens under legislation that has not yet been enacted?

Two reasons (at least).

First, from a policy perspective: Examining the operational and regulatory flows contemplated by pending legislation should surface potential problems with implementation and compliance before they become embedded in final rules. The legislative process benefits from practitioners stress-testing proposed frameworks against real-world token launch scenarios. Where the statutory text creates ambiguity, imposes unworkable requirements, or fails to account for common structures, identifying those gaps now, while the bills remain subject to amendment and conference, serves the broader goal of workable regulation.

Second, from a practitioner perspective: Clients, whether DevCos, foundations, or internal stakeholders(in the case of GCs) planning token projects operate on extended time horizons. A protocol beginning development today may not launch for 6-12+ months. Practitioners advising clients should understand how the regulatory landscape may look when the token is ready for distribution. If market structure legislation is enacted in some form, the token models most optimized for success will be those designed from inception to fit the eventual framework. Retrofitting is expensive; designing correctly from the outset is not. On a more fundamental level, clients always ask about important pending legislation (and there is no more important pending legislation than market structure)- specifically, how will such legislation impact their offering/operations—we should be able to provide a cogent answer.

With that framing, this Part II examines the issuance pathways available under both the House-passed CLARITY Act and the Senate Banking Committee substitute. Part I addressed the definitional framework—how a token qualifies as a non-security digital commodity. This Part addresses the next question: how does that token actually get into the hands of users?

Two Problems, One Framework

Part I established that both bills permit tokens to carry genuine economic rights: protocol fee distributions, governance-controlled treasury allocations, value appreciation tied to network growth—without becoming securities. The key is that those rights must flow from a decentralized governance system, not from promises by a centralized team or legal entity.

This framework addresses two distinct practical problems:

Problem 1: Launching New Tokens with Economic Rights

A protocol preparing to launch wants to issue tokens that carry real economic value from day one, or more likely, in the near-term on a tightly-moderated phase-in to decentralization. The token should entitle holders to a share of protocol fees, or governance rights over treasury deployment, or staking yields—”network equity” that gives holders a stake in the protocol’s success.

Under past and current regulatory uncertainty, many projects have avoided these structures entirely, issuing “governance-only” tokens with no direct economic rights. The pending legislation creates pathways to launch economically meaningful tokens without securities registration.

Problem 2: Adding Economic Rights to Existing Tokens

For the numerous protocols that have already issued tokens, most offerings have been in the form of governance tokens deliberately stripped of economic rights due to securities law concerns. These tokens may soon have the technical capability to activate fee sharing (the “fee switch”). And not just “fee sharing” in the circuitous value-accretion process of buyback/burn, but direct equity-like features in the form of true network dividends.

The pending legislation potentially unlocks these dormant economic rights. If the frameworks in Part I are enacted, existing protocols may be able to activate network revenue sharing, or add other economic features without transforming their tokens into securities.

The Unifying Principle

Both problems share the same solution: economic rights that flow from a qualifying decentralized governance system do not disqualify a token from non-security status.

For new(ish) launches, this means structuring token economics so that value flows from the protocol and its DGS, not from a foundation or development company.

For existing tokens, this means ensuring that the decision to add economic rights and the mechanism for distributing value both operate through decentralized governance—not centralized entity action.

The analysis below addresses both scenarios. Pathways 1 and 2A-C focus primarily on initial distribution of new tokens. The subsequent section addresses the specific mechanics of activating economic rights for tokens already in circulation.

The Issuance Problem

A token that qualifies as a digital commodity under the definitional frameworks discussed in Part I is not a security. But that classification doesn’t fully answer the issuance question. The sale of a digital commodity (particularly a sale by its issuer, for value, to raise capital) may still implicate securities law if the transaction itself constitutes an investment contract.

This is the residual Howey problem. Even if the token is a commodity, the transaction through which it is sold could be a security. Both bills address this through multiple pathways and requirements:

- Gratuitous / End User Distributions — distributions that are categorically not securities offerings

- Private Placement + Secondary Market — traditional exempt offerings followed by commodity-market secondary trading

- House Section 4(a)(8) Retail Exemption — direct-to-retail issuance with disclosure requirements

- Senate Regulation Crypto — SEC-mandated rulemaking for retail issuance

Each pathway has distinct requirements, limitations, and strategic implications.

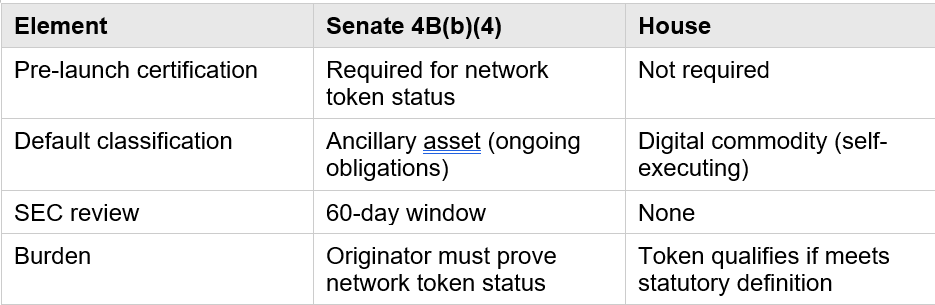

Critical Structural Difference: The Senate framework overlays two certification requirements on all issuance pathways:

● Section 4B(b)(4) “Prior Certification”: Determines whether your token is a “network token” (full non-security status) or “ancillary asset” (ongoing disclosure obligations). Without pre-issuance certification, all tokens are presumed to be ancillary assets.

● Section 104(d) “Certification of Non-Control”: Determines when insider sale restrictions lift. Available once the distributed ledger system is no longer under common control.

The House has no equivalent to either certification requirement—token classification is self-executing based on the statutory definition, and insider restrictions lift automatically upon Section 42 “mature blockchain” certification (which the issuer pursues, not submits for SEC approval).

A separate consideration: activating economic rights on existing tokens (the “fee switch”) operates differently because no new issuance occurs, and is addressed below.

Pathway 1: Gratuitous and End User Distributions

Both bills create a category of token distributions that are presumptively not securities offerings, allowing tokens to reach users—including retail—without registration or traditional exemptions.

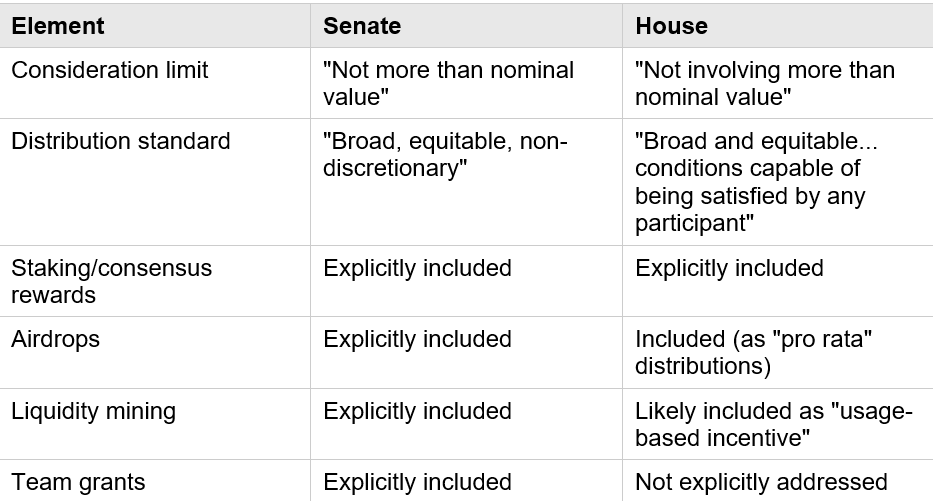

Senate: “Gratuitous Distribution”

The Senate bill defines “gratuitous distribution” at Section 2(8) as a distribution of a network token:

“in exchange for not more than a nominal value, distributed in a broad, equitable, and non-discretionary manner, including as— (A) a reward for participation in the consensus mechanism of the distributed ledger system; (B) a reward related to participation in or use of the distributed ledger system, including as staking rewards, so-called ‘airdrops,’ incentivized testnet rewards, or liquidity mining; (C) a programmatic distribution through the functioning of the distributed ledger system; or (D) as initial or ongoing distributions to founders, employees, or service providers for labor or services.”

Section 4B(b)(3) then provides the operative rule: “A gratuitous distribution of a network token shall be treated as not involving the offer or sale of a security.”

Key Elements:

- “Not more than a nominal value”: The recipient cannot pay meaningful consideration. Gas fees likely qualify as nominal; $100 “mint fees” likely do not.

- “Broad, equitable, and non-discretionary”: The distribution must be widely available and governed by objective criteria—not hand-picked recipients at issuer discretion.

- Enumerated safe harbors: Staking rewards, airdrops, liquidity mining, testnet incentives, and programmatic distributions are explicitly included.

- Team/service provider distributions: Notably, distributions to “founders, employees, or service providers for labor or services” qualify. This is significant—it suggests vesting token grants to team members are not securities offerings if structured as gratuitous distributions.

House: “End User Distribution”

The House bill defines “end user distribution” at Section 2(a)(27) of the Securities Act (as amended) as a distribution:

“not involving more than a nominal value, distributed in a broad and equitable manner based on conditions capable of being satisfied by any participant in the blockchain system, including: (A) a reward for participation in the consensus mechanism of the blockchain system; (B) a user or usage-based incentive...; (C) an initial or early distribution that is pro rata to all participants that have satisfied the conditions of the distribution...”

Section 202(a) provides: “An end user distribution shall not be treated as a sale under the Securities Act of 1933, the Securities Exchange Act of 1934, or the Investment Company Act of 1940.”

Key Elements:

- “Conditions capable of being satisfied by any participant”: This is slightly more prescriptive than the Senate’s “non-discretionary” standard. The conditions must be generally attainable—not gated by invitation, accreditation, or issuer selection.

- No explicit team carveout: Unlike the Senate, the House definition does not explicitly include distributions to founders/employees/service providers. This creates ambiguity about whether team token grants qualify as end user distributions or require separate analysis.

Critical Issue: Gratuitous Distributions Under the Senate Framework

The interaction between the Senate’s gratuitous distribution exemption and the ancillary asset presumption creates significant ambiguity for new projects.

The Statutory Architecture

The Gratuitous Distribution Exemption

Section 4B(b)(3) provides: “A gratuitous distribution, by itself, shall be presumed to not constitute an offer or sale of a security.”

The Definition Problem

Section 4B(a)(4) defines “gratuitous distribution” as “a distribution of a network token...” The exemption is expressly limited to network tokens.

The Certification Gap

Section 4B(b)(4) provides that all network tokens are “presumed” to be ancillary assets unless the originator submits certification. That certification requires the Section 4B(d)(3)(C)(i) statement—which includes a one-year lookback (more on this lookback, below) showing nominal entrepreneurial/managerial efforts.

New projects cannot satisfy this lookback. They cannot certify.

The Ambiguity: Can New Projects Do Exempt Gratuitous Distributions?

Reading 1: Ancillary Assets Are Network Tokens (Exemption Applies)

The definition of “ancillary asset” in Section 4B(a)(1) is: “a network token, the value of which is dependent upon the entrepreneurial or managerial efforts...”

Ancillary assets are a subset of network tokens—network tokens that haven’t been certified as free from issuer dependence. Under this reading:

- Gratuitous distribution = distribution of network token

- Ancillary asset = network token (with issuer dependence)

- Therefore: gratuitous distribution of ancillary asset = gratuitous distribution of network token

- Therefore: exemption applies

Reading 2: Exemption Was Designed for Certified Network Tokens (Gap Exists)

The statutory architecture suggests the gratuitous distribution exemption was designed for tokens that have achieved—or will achieve—network token certification:

- The definition references “network token” as a term of art

- The certification framework distinguishes “network tokens” (certified) from “ancillary assets” (uncertified)

- The exemption may have been drafted assuming the distributing token would eventually be certified

Under this reading, gratuitous distributions of tokens that cannot be certified exist in a regulatory gap.

What’s Clear vs. What’s Ambiguous

Likely Clear:

- The distribution itself is not an “offer or sale” under Section 4B(b)(3), regardless of whether the token is an ancillary asset or certified network token. The exemption is for the transaction type, not the token status.

- Related persons holding ancillary assets face Section 104(c) sale restrictions, regardless of how they acquired the tokens.

Ambiguous:

- Do 4B(d) disclosures apply to gratuitous distributions of ancillary assets? Section 4B(c)(1) triggers disclosure requirements for distributions “pursuant to Regulation Crypto... or an effective registration statement.” Gratuitous distributions are pursuant to neither. This suggests 4B(d) disclosures may NOT apply to gratuitous distributions—even of ancillary assets. But Section 4B(c)(4) requires disclosures for “resales” following private placement exemptions. Does a gratuitous distribution followed by recipient resales trigger this provision?

- What happens when recipients resell? If the initial distribution doesn’t trigger 4B(d) disclosures, but resales require “current public information” under 4B(c)(4), there’s a timing problem: disclosures would need to be furnished before recipients can resell, even though no disclosure was required at distribution.

- Does the exemption extend to all consequences of ancillary asset status? Even if the distribution is exempt from being an “offer or sale,” the distributed tokens are still ancillary assets. Are they subject to all ancillary asset rules (disclosure, insider restrictions) or only some?

Conservative Approach

Given the ambiguity, conservative practitioners should:

- Assume 4B(d) disclosures apply. Even if the statute doesn’t clearly require them for gratuitous distributions, furnishing disclosures eliminates uncertainty about recipient resales.

- Structure related person allocations carefully. Team grants are subject to 104(c) restrictions regardless of distribution method.

- Document the gratuitous nature thoroughly. Ensure distribution meets all requirements (nominal value, broad/equitable, non-discretionary) to maximize exemption arguments.

- Plan for certification timeline. Build toward 4B(b)(4) certification to exit ancillary asset status as quickly as possible.

Key Insight: Under the House framework, token classification is self-executing—if the token meets the definition, it’s a digital commodity. Under the Senate framework, all tokens are presumed to be ancillary assets until certified, creating regulatory overhang even for exempt distributions.

Practitioner notes:

Until rulemaking or guidance clarifies, new projects planning gratuitous distributions under a Senate-framework world should:

- Comply with 4B(d) disclosures prophylactically, even if not clearly required

- Build the one-year track record needed for eventual 4B(b)(4) certification

- Structure distributions to clearly satisfy the gratuitous distribution definition

- Ensure related persons understand and comply with 104(c) restrictions

- Consider whether the House framework’s cleaner treatment justifies advocacy for House-style provisions in conference

This is a genuine statutory gap that conference negotiation or SEC rulemaking will need to address.

Comparative Analysis

Practical Challenges

Challenge 1: What is “nominal value”?

Neither bill defines “nominal.” Is $1 nominal? $10? Does it depend on the value of the token received? The term likely imports concepts from gift tax and contract law, where nominal consideration means consideration so small it cannot reasonably be viewed as bargained-for exchange. Gas fees and de minimis participation requirements (completing a tutorial, joining a Discord) likely qualify. Meaningful “mint prices” or purchase requirements likely do not.

Practitioner note: Structure distributions to require no payment or only incidental costs (gas, network fees). Avoid any pricing that could be characterized as purchase consideration.

Challenge 2: Airdrop Eligibility Criteria

“Broad and equitable” and “non-discretionary” requirements constrain how projects can target airdrops. Restricting eligibility to early users, high-volume traders, or specific wallet addresses is likely permissible if based on objective, verifiable onchain criteria. Hand-selecting recipients based on relationships or subjective assessments is likely not.

Practitioner note: Document eligibility criteria in advance. Use objective, onchain metrics. Avoid discretionary “grants committees” for broad distributions.

Challenge 3: Team Grants Under the House Bill

The Senate explicitly permits gratuitous distributions to “founders, employees, or service providers.” The House does not. This creates risk that team token grants under the House framework require separate exemption analysis (potentially Rule 701 for employees, Regulation D for advisors/service providers).

Practitioner note: Under the House framework, consider structuring team grants through traditional exemptions rather than relying on the end user distribution pathway. Under the Senate framework, team grants appear covered—but should still satisfy the “broad, equitable, non-discretionary” standard (e.g., pursuant to a published token allocation plan, not ad hoc grants).

Challenge 4: Liquidity Mining Characterization

Both bills contemplate liquidity mining as a qualifying distribution. But liquidity mining involves users providing something (liquidity) in exchange for tokens. Is that “nominal value”? The answer likely depends on whether the tokens are compensation for a service (providing liquidity to the protocol) rather than payment for purchasing tokens. The bills appear to treat liquidity mining as the former—incentivizing protocol participation rather than raising capital.

Practitioner note: Frame liquidity mining as user incentives for protocol participation. Avoid structures where LP token deposits are characterized as “purchasing” governance tokens.

Pathway 2: Sales for Value

When a project sells tokens (whether to accredited investors, retail purchasers, or both) it is generally conducting an offering. The transaction must fit within a securities exemption, and the regulatory consequences depend on which bill governs and which exemption is used.

Three primary mechanisms exist for selling tokens:

● 2A: Private Placement: Reg D/Reg S sales to accredited/offshore investors (both bills)

● 2B: House Retail Exemption: Section 4(a)(8) sales to retail with BD intermediary (House only)

● 2C: Senate Regulation Crypto: SEC-mandated retail framework for ancillary assets (Senate only)

All three are fundamentally the same activity (selling tokens for value under an exemption) but with different investor pools, disclosure requirements, and regulatory consequences.

The Fundamental House/Senate Divide

Before examining each mechanism, understand the structural difference:

House: Token classification is self-executing. If a token meets the digital commodity definition, it is a digital commodity, regardless of how it was sold. After the offering, secondary sales by non-issuers are commodity transactions. The issuer has no ongoing disclosure obligations solely by virtue of having sold tokens.

Senate: All tokens are presumed to be ancillary assets unless the originator obtains Section 4B(b)(4) certification of network token status. But that certification requires a one-year track record of nominal issuer involvement, meaning that new projects cannot certify at launch. For practical purposes, any tokens sold by new projects under the Senate framework will be ancillary assets subject to ongoing 4B(d) disclosure obligations, regardless of which sales mechanism used.

This is the critical insight: under the Senate framework, the choice between private placement, Regulation Crypto, or any other mechanism doesn’t change your ancillary asset status. You’re in the ancillary asset regime until you can satisfy the certification requirements, which takes at least a year.

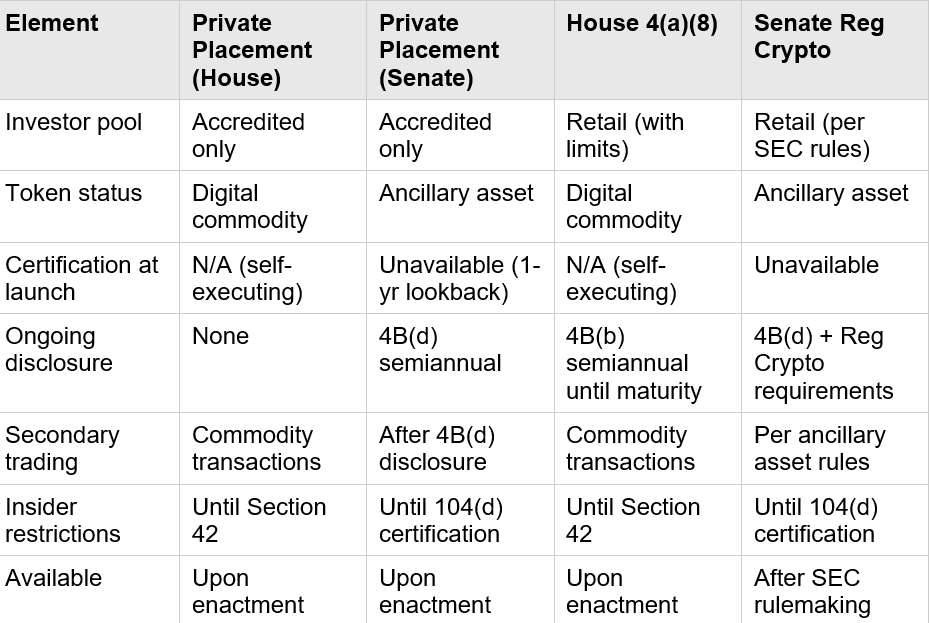

2A: Private Placement (Reg D/Reg S)

Both frameworks preserve the traditional path: sell tokens via private placement to accredited/sophisticated investors, then allow those tokens to trade on secondary markets.

The Structure

Step 1: Sell tokens through Regulation D (Rule 506(b) or 506(c)) to U.S. accredited investors, and/or Regulation S to offshore investors. The transaction is a securities offering with all attendant requirements: accredited investor verification, Form D filing, etc.

Step 2: Tokens enter circulation and may trade on secondary markets.

Step 3: Classification and ongoing obligations depend on which framework governs.

House Treatment

Section 203 provides that secondary sales of digital commodities by non-issuers “shall be deemed not to be an offer or sale of such investment contract.” The House severs the token from the investment contract. Once in secondary hands, it trades as a commodity.

- No ongoing issuer disclosure requirements

- Related persons face sale restrictions until Section 42 “mature blockchain” certification

- Ordinary secondary holders can trade freely

Senate Treatment

Network token certification is unavailable at launch (requires one-year lookback-more below). The token is therefore an ancillary asset, triggering:

Section 4B(d) Disclosure Requirements: Initial disclosures prior to resale eligibility, then semiannual disclosures including:

- Description of the ancillary asset and distributed ledger system

- Development plans and roadmap

- Related person identification and token holdings

- Material contracts and risk factors

- Source code and technical specifications

- Use of proceeds

Section 104(c) Insider Restrictions: Related persons may sell only if disclosures are current, minimum holding periods are satisfied (12 months for pre-enactment tokens; 6 months + volume limits for post-enactment tokens), and sales occur through compliant channels.

Secondary Market Treatment: Section 4B(b)(2)’s safe harbor applies to “network tokens” not ancillary assets. Secondary sales of ancillary assets by non-related persons appear permissible once 4B(d) disclosures are furnished, but the statutory treatment is less explicit.

Path to Network Token Status

- After 12+ months of operational history with nominal issuer involvement:

- Submit Section 4B(b)(4) certification with (d)(3)(C)(i) statement

- Wait 60 days (negative consent)

- Upon effectiveness, ongoing 4B(d) disclosure obligations terminate

- Section 104(c) restrictions continue until Section 104(d) certification of non-control

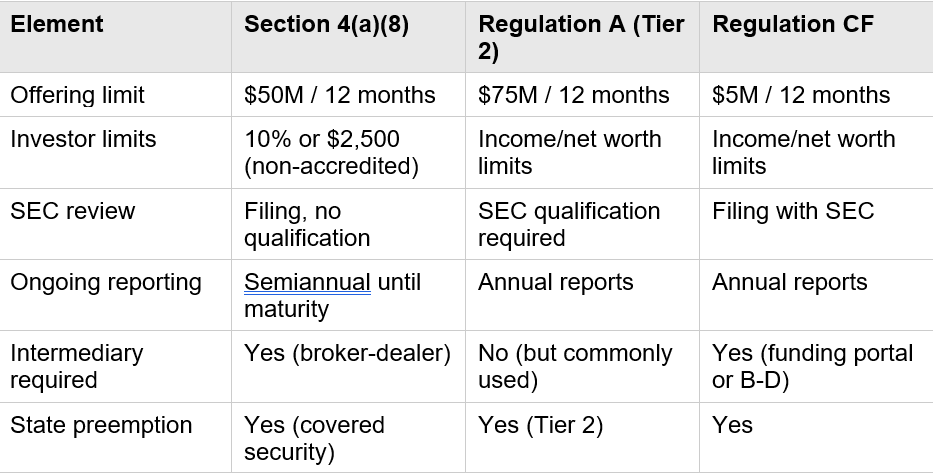

2B: House Retail Exemption — Section 4(a)(8)

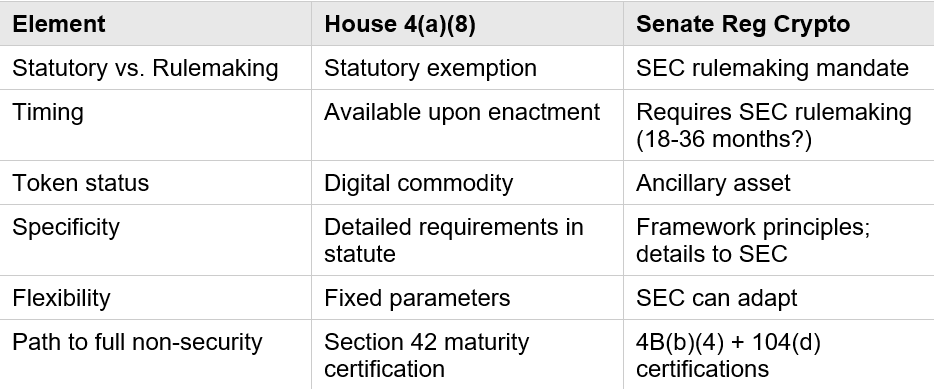

The House creates a purpose-built exemption for direct-to-retail token sales—something that doesn’t exist under current law or the Senate framework.

The Structure

New Section 4(a)(8) of the Securities Act exempts offers and sales of investment contracts involving digital commodities if:

Maturity Intent: The blockchain system is either already certified as mature, OR the issuer intends for it to become mature within 4 years (subject to extensions).

Offering Limits:

- $50 million maximum aggregate proceeds in any 12-month period

- No single purchaser may acquire more than 10% of the offering (or $2,500, whichever is greater) unless accredited

Disclosure Requirements: Section 4B(b) mandates extensive disclosures filed with the SEC, including:

- Digital commodity and blockchain system description

- Development roadmap and plan to achieve maturity

- Source code and technical specifications

- Token economics (supply, allocation, mechanisms)

- Ownership disclosures (related persons, affiliated persons)

- Risk factors

- Use of proceeds

- Ongoing semiannual reporting until maturity

Sales Through Registered Intermediaries: Offers and sales must be conducted through a registered broker-dealer that is a member of a national securities association (i.e., FINRA member).

Disqualification Provisions: Bad actor disqualification rules apply.

Comparison to Existing Exemptions

Consequences of Failure to Mature

If the blockchain doesn’t achieve Section 42 maturity certification within 4 years:

- No additional exempt offerings without SEC qualification

- Enhanced disclosure obligations

- Insider restrictions continue indefinitely

- The token does not appear to lose digital commodity status—but issuer capital-raising ability is severely constrained

Practical Challenges

Broker-Dealer Requirement: All 4(a)(8) sales must go through a registered broker-dealer. Which BDs will participate? How will compliance integrate with on-chain distribution? The infrastructure is nascent.

Ongoing Reporting Burden: Semiannual reports until maturity—potentially more extensive than Regulation A requirements.

Four-Year Runway: Realistically assess decentralization timeline before relying on 4(a)(8).

2C: Senate Retail Access — Regulation Crypto

The Senate takes a different approach to retail: rather than a statutory exemption, it mandates SEC rulemaking. And importantly, Regulation Crypto is explicitly designed for ancillary assets (tokens that have not achieved network token certification).

The Mandate

Section 103 requires the SEC to adopt “Regulation Crypto” providing:

“an optional regulatory framework governing the offer and sale of an ancillary asset that is intended to be a network token, as part of a registered offering or an offering exempt from registration, including provisions that—”

Required provisions include:

- Regulatory pathway for retail sales consistent with investor protection

- Tailored disclosure requirements (technical, governance, tokenomics)

- Resale limitations for related persons

- Periodic disclosure obligations

- Framework for transition to non-security status upon decentralization

Key Insight: Regulation Crypto Is for Ancillary Assets

Note the statutory language: Regulation Crypto governs “ancillary assets.” This isn’t an alternative to ancillary asset status, it is the retail access mechanism within the ancillary asset regime.

A project using Regulation Crypto:

- Is an ancillary asset issuer (by definition)

- Must comply with Section 4B(d) disclosure requirements

- Has related persons subject to Section 104(c) restrictions

- May eventually pursue 4B(b)(4) certification when the one-year lookback can be satisfied

Comparison to House 4(a)(8)

Practical Challenges

Rulemaking Timeline: Regulation Crypto doesn’t exist until the SEC develops it. Realistic timeline: 18-36 months post-enactment.

SEC Discretion: The statute provides principles and the SEC fill in the details. Uncertainty to persist in the interim with respect to what Reg Crypto will actually require.

Layered-on Ancillary Asset Regime: Reg Crypto isn’t an escape from ancillary asset status (that would be the gratuitous distribution of a network token, noted above); rather, it is the retail distribution regime for ancillary assets.

Comparative Summary: All Sales Mechanisms

Common Practical Challenges (All Sales Mechanisms)

Challenge 1: The Senate’s Mandatory Disclosure Period

Under the Senate framework, regardless of which sales mechanism you use, you face a mandatory disclosure period. The 4B(b)(4) certification requires a one-year track record—so every new project starts as an ancillary asset.

Practitioner note: For Senate-framework planning, budget for at least 12-18 months of 4B(d) compliance. Build disclosure infrastructure from day one. The question is not whether to accept ancillary asset status, but how long it will last.

Challenge 2: What Constitutes “Nominal” Efforts?

The Senate certification requires demonstrating “not more than a nominal level of entrepreneurial or managerial efforts” over the preceding year. Key questions:

- Does ongoing protocol development count?

- What about marketing, business development, or exchange listings?

- Does active governance participation by the foundation count?

Practitioner note: Document the transition to decentralized operations. Track when functions transfer from originator to community.

Challenge 3: “Essential Promises Fulfilled”

The statute suggests that incomplete roadmaps or unfulfilled commitments may preclude certification.

Practitioner note: Be careful about public commitments. Consider what constitutes an “essential promise” versus aspirational goals.

Challenge 4: Originator/Issuer Sales

Both bills restrict secondary market treatment to sales by non-issuers. The originator cannot simply sell into the secondary market and claim commodity treatment (House) or non-security treatment (Senate).

Practitioner note: Plan for extended issuer lockups until maturity/decentralization certification.

Challenge 5: “Agent or Underwriter” Scope

Both bills exclude sales by “agents or underwriters” from secondary market safe harbors. Who qualifies? Market makers? Exchanges with token grants? Advisory firms paid in tokens?

Practitioner note: Assume any entity with a distribution relationship may not benefit from secondary market safe harbors.

Challenge 6: Integration with Gratuitous Distributions

If the issuer conducts both sales and gratuitous distributions, are they “integrated”? Both bills appear to treat gratuitous distributions as categorically not offerings—which should preclude integration.

Practitioner note: Structure and document sales and distributions as separate programs with distinct purposes.

Senate Certification Requirements: The Overlay on All Pathways

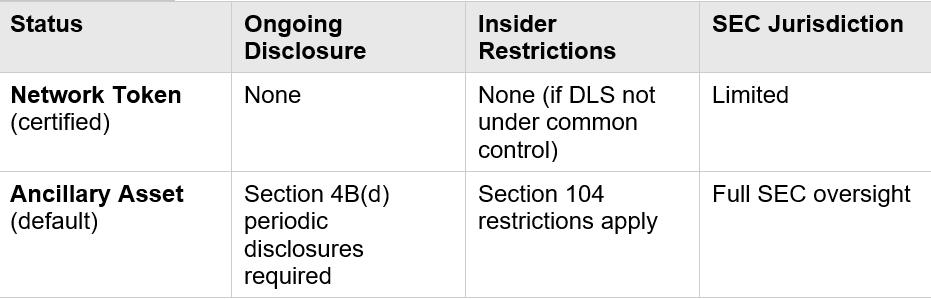

The Senate framework imposes two certification requirements that apply across all issuance pathways—gratuitous distributions, private placements, and Regulation Crypto offerings alike. These are not separate issuance paths; they are compliance layers that determine a token’s regulatory status and the restrictions applicable to insiders.

Certification #1: Section 4B(b)(4) “Prior Certification”: Network Token vs. Ancillary Asset

This certification determines whether your token achieves full “network token” status (outside securities law) or remains an “ancillary asset” (subject to ongoing SEC obligations).

The Ancillary Asset Presumption

Section 4B(b)(4)(A) establishes a rebuttable presumption:

“For purposes of this section, there shall be a rebuttable presumption that a network token, including a network token distributed in the manner described in paragraph (3) [gratuitous distributions], is an ancillary asset unless the originator of that network token submits to the Commission a completed written certification, supported by reasonable evidence, as defined by the Commission, sufficient to demonstrate that the network token is not an ancillary asset.”

Why It Matters

An “ancillary asset” is a token in regulatory purgatory—on a path to becoming a network token, but not there yet. The originator must furnish ongoing disclosures (similar to public company reporting), and related persons face sale restrictions.

A certified “network token” is fully outside the securities laws—no ongoing disclosure, no insider restrictions (assuming the DLS is decentralized).

The Certification Process

- Submission: Originator submits written certification to SEC stating the token is not an ancillary asset, supported by “reasonable evidence” (as defined by SEC rules)

- 2. 60-Day Negative Consent: Certification becomes effective on the earlier of:

- SEC notification of no objection, or

- 60 days after submission (if SEC has not denied)

- SEC Denial (if any): Permitted only during the 60-day window; requires 10-day notice, opportunity for written and oral submissions by interested persons, and Commission vote to deny based on finding of disqualifying rights under Section 4B(a)(6)(B). Denial is final agency action, appealable to court.

- Designated SEC Office: SEC must designate an office to acknowledge receipt, provide guidance, and route certifications.

Comparison to House

The House has no equivalent. Under the House framework, a token meeting the “digital commodity” definition is a digital commodity—full stop. Classification is self-executing. The issuer makes its own determination based on statutory criteria with no mandatory SEC pre-clearance.

Strategic Choice: Certify or Accept Ancillary Asset Status?

Not every protocol must pursue network token certification immediately. A protocol comfortable with ongoing Section 4B(d) disclosures might:

- Launch as an ancillary asset under Regulation Crypto

- Build toward decentralization over time

- Pursue certification when confident in approval

For protocols with clear network token characteristics and mature decentralization, immediate certification is likely worthwhile. For early-stage protocols with arguable characteristics, ancillary asset status with a path to certification may be more practical.

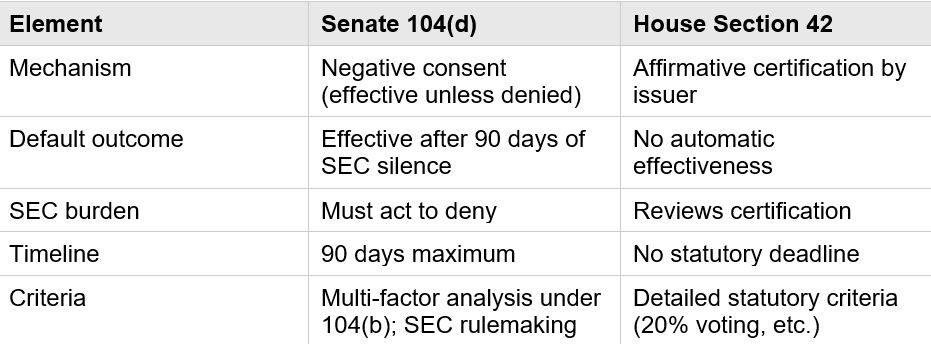

Certification #2: Section 104(d) — Certification of Non-Control (Decentralization)

This certification determines when insider sale restrictions lift. It applies to both network tokens and ancillary assets—the question is whether the distributed ledger system is still under common control by related persons.

The Certification Process

Submission: A “certification covered party” (originator, subsidiary, related person, or commonly controlled entity) submits written certification that the DLS is “not under the common control of related persons,” supported by reasonable evidence consistent with Section 104(b) criteria.

90-Day Negative Consent: Certification becomes effective on the earlier of:

- SEC notification of no objection, or

- 90 days after submission (if SEC has not denied)

SEC Denial (if any): Permitted only during the 90-day window (or upon material change in circumstances); requires 10-day notice, hearing before the Commission, and vote to deny. Denial is final agency action.

Why It Matters

Until the DLS is certified as not under common control:

● Related persons face sale restrictions under Section 104(c)

● Pre-certification sales require ongoing 4B(d) disclosures, minimum holding periods, and volume limitations

● Post-certification sales have reduced restrictions

Comparison to House Section 42

The Senate’s negative consent approach is arguably more favorable to issuers: the burden shifts to the SEC to act within 90 days, providing timeline certainty.

Putting the Certifications Together

Under the Senate framework, a protocol’s journey looks like this:

Launch Phase:

- Choose issuance pathway (gratuitous, private placement, Reg Crypto)

- Decide whether to pursue 4B(b)(4) certification (network token) or accept ancillary asset status

- If seeking network token status: submit certification, wait 60 days

- If accepting ancillary asset status: comply with 4B(d) disclosures from launch

Operations Phase:

- Network tokens: minimal ongoing obligations

- Ancillary assets: semiannual disclosures under 4B(d); insider restrictions under 104(c)

Decentralization Phase:

- When DLS is no longer under common control: submit 104(d) certification

- Wait 90 days for effectiveness

- Upon effectiveness: insider restrictions lift; related persons can sell freely (subject to any remaining conditions)

Enabling Network Equity: Navigating the DGS Carveout

As discussed in Part I, both bills treat qualifying economic rights that flow from a decentralized governance system (DGS) as non-securities. This is the statutory overlay that makes network equity possible.

Senate Section 4B(a)(6)(B)(ii):

“[A network token] shall not be disqualified from being deemed a network token due to the granting of economic interests or voting capabilities with respect to a distributed ledger system or its decentralized governance system...”

House Section 2(a) “Digital commodity” definition: The definition excludes tokens providing financial interests “from a person”—but the DGS carveout clarifies that interests from a decentralized governance system are not interests “from a person.”

The logic: when economic rights flow from decentralized, programmatic systems governed by token holders themselves, there is no “issuer” in the traditional sense. The fourth Howey prong—profits from the efforts of others—breaks down when the “others” are the token holders collectively acting through governance.

What This Means Practically

A token can include, from day one (but may not be practical for most protocols) or added later:

Revenue Distribution Rights

- Pro-rata share of protocol fees

- Staking yields funded by protocol revenue

- Buyback programs funded by treasury

Governance Rights

- Voting on protocol parameters

- Voting on fee structures

- Voting on treasury deployment

Economic Participation Rights

- Rights to future airdrops

- Priority access to protocol features

- Discounts on protocol services

- All of these can attach to tokens without triggering securities classification if they flow from a qualifying DGS.

Requirements for a Qualifying DGS

The carveout isn’t automatic. The governance system must actually be “decentralized.” Key requirements:

1. No Single Point of Control

The DGS cannot be controlled by the originator, foundation, or any coordinated group. Both bills use variations of “common control” tests:

- Senate: DLS must not be “under common control of one or more related persons”

- House: Blockchain must qualify as “mature” (no person/group controls 20%+ of voting power)

Practical implication: If the foundation controls 40% of governance tokens, economic rights flowing from “governance votes” are really flowing from the foundation. The carveout likely doesn’t apply.

2. Programmatic Implementation

Economic rights must be implemented through smart contracts, not entity discretion:

- ✓ Smart contract that automatically distributes fees to stakers

- ✓ Governance vote that triggers on-chain parameter change

- ✗ Foundation that “decides” to distribute revenues quarterly

- ✗ Committee that selects buyback timing and amounts

Practical implication: The mechanism matters as much as the governance vote. A governance vote authorizing a foundation to make distributions at its discretion doesn’t qualify—the distribution itself must be programmatic.

3. Genuine Decentralization of Decision-Making

The governance process must involve actual distributed decision-making:

- Broad token distribution (not concentrated in insiders)

- Meaningful participation thresholds

- Transparent proposal and voting processes

- No veto rights retained by originators

Practical implication: A “governance system” where the foundation holds 51% and rubberstamps its own proposals isn’t decentralized governance—it’s centralized control with extra steps.

When Can Economic Rights Attach?

Option 1: At Launch

Tokens can be issued with economic rights from day one, provided:

- The DGS is operational at launch

- The DGS meets decentralization requirements at launch

- Economic rights flow programmatically from the DGS

This is challenging (if not impossible) for most new projects. At launch, tokens are typically concentrated (team, investors, foundation), and the governance system may not yet be meaningfully decentralized.

Practitioner note: If launching with economic rights, ensure:

- Initial token distribution is sufficiently broad

- No single party or coordinated group controls governance

- Revenue distribution mechanisms are fully on-chain

- Governance cannot be overridden by originator veto

Option 2: Post-TGE Activation (The “Fee Switch”)

Tokens can be issued without economic rights initially, then economic rights can be activated later via DGS governance. This is the “fee switch” model.

Advantages:

- Tokens can be issued while governance is immature/centralized

- Economic rights activate only when DGS is genuinely decentralized

- Cleaner securities analysis at issuance (no economic rights = fewer Howey factors)

Practitioner note: Consider structuring the activation so that:

- The decision to activate is made by DGS vote, not originator

- The mechanism is programmatic (smart contract upgrade, not entity action)

- Activation occurs only after meaningful decentralization

- Document the governance process contemporaneously

Option 3: Phased Economic Rights

Some economic rights can exist at launch (e.g., governance voting, protocol fee discounts), with additional rights (e.g., revenue sharing) activated later as decentralization matures.

Practitioner note: Map each economic right to its activation trigger and DGS qualification requirements.

What the DGS Carveout Does NOT Protect

The carveout is powerful but not unlimited:

Rights from Entities, Not DGS

- Dividends from a corporate treasury (even if “approved” by governance)

- Revenue sharing from off-chain business operations

- Promises of future value from the development team

Governance Theater

- “Governance” where the foundation always controls outcome

- Advisory votes with no binding effect

- Governance subject to originator veto

Centralized Distribution Mechanisms

- Foundation-administered airdrops (even if governance-approved)

- Discretionary treasury distributions

- Off-chain revenue sharing agreements

Key principle: The carveout protects economic rights that are structurally decentralized—not rights that are merely labeled as flowing from governance.

Interaction with Issuance Pathways

The DGS carveout affects issuance strategy:

Gratuitous Distributions (Pathway 1)

- Tokens with economic rights can be distributed gratuitously

- Economic rights don’t convert a gratuitous distribution into a sale

- But issuer must qualify as DGS

Sales for Value (Pathway 2)

- Tokens with economic rights can be sold under exemptions

- The transaction may be an investment contract even if the token isn’t a security

- Post-sale, secondary trading is commodity trading (House) or non-security (Senate network tokens)

Senate Ancillary Asset Regime

- Tokens with economic rights are still subject to ancillary asset presumption

- DGS carveout affects token classification, not certification requirements

- Must still pursue 4B(b)(4) and 104(d) certifications

Conclusion: Preparing for an Uncertain but Directionally Clear Future

The specific statutory text will evolve. Conference negotiations may alter thresholds, timelines, and requirements. Agency rulemaking will fill gaps—sometimes in unexpected ways.

But the directional framework is increasingly clear:

1. Tokens with genuine utility and economic rights can exist outside securities law: if those rights flow from decentralized systems rather than centralized issuers.

2. Two fundamental pathways exist: gratuitous distributions (not offerings) and sales for value (offerings requiring exemptions). The regulatory consequences depend on which you choose and which framework governs.

3. The Senate imposes a mandatory disclosure period that the House does not. Under the Senate framework, the 4B(b)(4) certification requires a one-year track record of nominal issuer involvement—meaning new projects cannot certify at launch. Every new Senate project starts as an ancillary asset with ongoing 4B(d) disclosure obligations, regardless of which sales mechanism it uses. The House has no equivalent; classification is self-executing.

4. Existing tokens can evolve. The frameworks contemplate that tokens can acquire economic rights post-launch: the fee switch can be activated, buybacks can be implemented, staking yields can be enabled— all without becoming securities, provided those rights flow from qualifying decentralized governance.

5. Both frameworks require a path to decentralization, but with different mechanics. The Senate’s 104(d) certification (90-day negative consent) is more favorable than the House’s Section 42 process (no statutory deadline).

6. Conservative structuring from inception pays dividends. Designing for the strictest plausible interpretation—sub-20% coordinated control, genuine DGS governance, programmatic value mechanisms—positions projects to succeed under either framework.

Practitioners advising clients today should map token models against these frameworks now. The projects that launch cleanly under eventual legislation—and the existing protocols that successfully activate economic rights—will be those designed with these frameworks in mind.

The era of “launch and hope” is coming to a close. The era of “design for compliance” is dawning. The topics discussed and frameworks examined in these articles aim to provide a blueprint.

This is Part II of a three-part series on network equity under pending market structure legislation. Part I addressed the definitional framework; this Part addressed issuance pathways, certification processes, and post-TGE activation of economic rights. Part III will set forth a decision framework, a DGS checklist and five model approaches to token issuance and will be available under a soon-to-be-announced paid sub tier intended for professional advisors (note: 100% of sub revenue will be donated to crypto advocacy groups).